2017 Online Banking Customer Service Trends

Online banking has gone a long way since the early 2000s and now that it’s 2017, there are a lot of exciting new developments that we may not have expected then. But despite how online banking has evolved these past years, the expectations remain the same. In its Digital IQ Survey, PwC showed that growing revenue is still the main drive for digital investments such as online banking.

While it’s true that generating revenue is a good driver for digital investments, this shouldn’t be the only use of digital banking innovations. These investments need to be focused on improving customer service on whole.

On that note, let’s discuss some of the new customer service trends we are beginning to see in online banking in 2017:

1. New Ways To Digitize Branches

We are beginning to see more creative ways to bring more technology into branches and even creating a closer link between mobile and online banking along with traditional banking. Some services we’ve seen include being able to start applications through mobile and online banking and continuing them in banks. Another interesting development we’ve heard of is abolishing teller counters in favour of free-roaming bank tellers with tablets who interact with clients in a lounge instead of a waiting lobby.

Being able to create this seamless connection between online and brick-and-mortar banking requires plenty of integration work across the bank’s processes and systems.

2. Mobile Payments On The Rise

Mobile wallets are continuing to spread globally as more retailers are willing to accept them as a payment method. Even Italy saw the launch of Apple Pay this year supported by banking giant Unicredit at the end of the first quarter along with Carrefour Banca. We can only expect more banks to follow suit given the younger generation’s propensity for using smartphones to efficiently manage their lives and their future financial influence.

But why are banks going for mobile payments? It’s all part of providing more flexibility for customers. More payment options is just another way to improve your service to your customers by increasing convenience for them.

3. More Advanced Data From Online Customers

Banks that put a particular focus on their online presence, especially their websites are going to gather more advanced data from online customers such as their habits while they’re on the online banking portal as well as getting deeper insights into customer needs.

Functionalities such as co-browsing, which allows banks to see firsthand exactly how customers use their website will be useful in improving online banking services. An MX Consumer Survey revealed that 67% of banking customers put “a simple and easy digital banking experience” as a key factor in choosing a bank or credit union vs. only 33% who “preferred friendly and helpful tellers and call staff”.

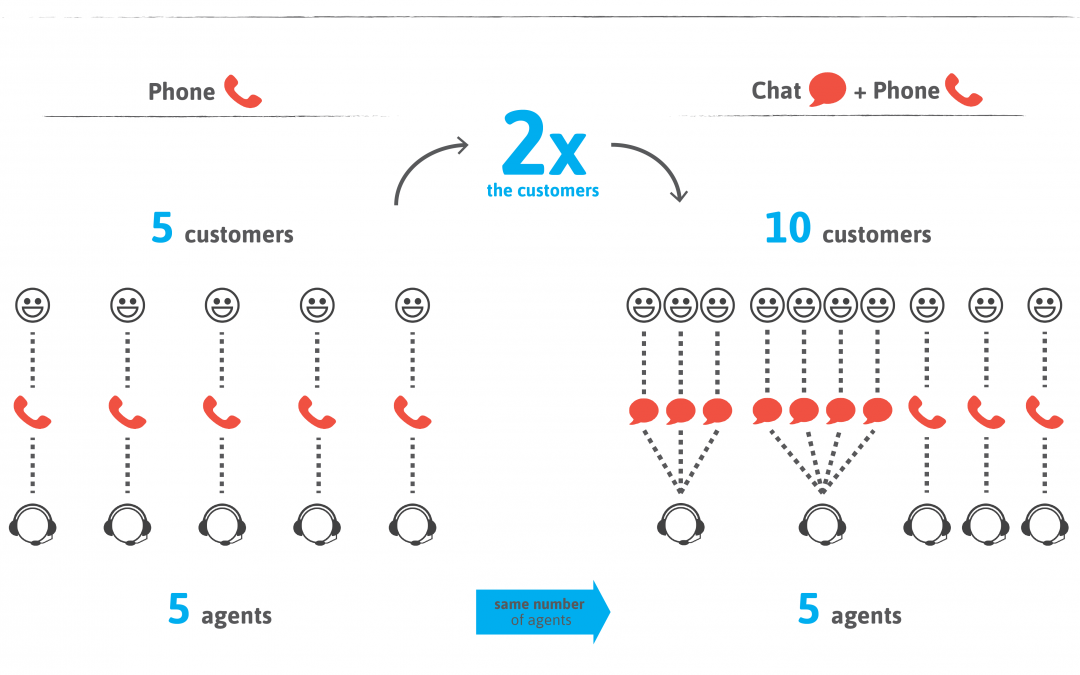

4. Increasing Personal Interactions in Online Banking

The steady increase in the rise of online banking use is not because people are shying away from personal contact. It’s just a faster way of getting their things done. However, there’s a huge opportunity to improve online banking services by adding the same element of personalized interaction that’s provided by bank tellers and customer service representatives.

On-demand chat functionalities with live customer service representatives can help clarify any doubts customers may have when it comes to certain online banking procedures or even just understanding certain complex financial terms.

5. Customer Service Still Key To Digital Banking Success

Accenture’s Banking Customer 2020 trends report says that in reality, most of any bank’s customers are “digital banking customers” one way or another. “Digital-only” banking users are up at 20% with traditional banking customers still using digital channels every now and then. Online banking services have also increased number of total interactions. In fact, 61% of banking customers expect to increase their online interactions across their lifecycle.

This then presents a potential risk (or opportunity) for financial institutions. Up to 80% of clients who switched banks did so because of poor customer service and said that if their issues would have been resolved, then they would have stayed on as a customer. Online banking without proper customer support is a risk that could be addressed through additional customer service functionalities such as on-demand chat, intelligence assistants, or even chatbots.

Conclusion

There’s no doubt that online banking will continue to grow in importance as younger generations increase their financial influence globally. Generation Z and Millennials are some of the most mobile and technologically-savvy customers that banks ever had and will expect a lot from digital banking services in the form of top-notch customer service. Financial institutions need to make sure to put customer service and customers at the heart of all its online banking changes as they move forward.